Early Retirement: Why Parents Have Doubts About Its Effectiveness and Fairness

Invest4Kids survey of 2,400 parents reveals a clear need for reform

The Early Start Pension is designed to help children build wealth at an early age and strengthen their retirement savings in the long term. But what do parents really think of this model? A recent survey by Invest4Kids of 2,400 parents paints a clear picture. In its current form, the Early Start Pension is met with significant skepticism regarding both its effectiveness and fairness.

Early Retirement: Is €10 a Month Enough to Build Wealth?

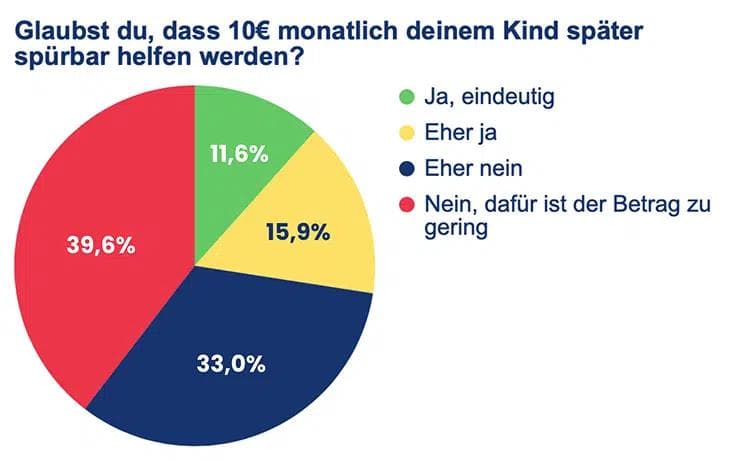

Figure 1: Parents’ assessment of the impact of the early retirement pension

A key finding of the survey concerns the amount of government assistance. 72.6 percent of the parents surveyed do not believe that the planned 10 euros per month will make a noticeable difference for their child in the future. Just under 40 percent consider the amount to be clearly too low, while another 33 percent express significant doubts. Only 27.5 percent see any real benefit at all.

From an economic perspective, this is problematic. Sustainable wealth accumulation relies on time, sufficient contributions, and the power of compound interest. Many parents apparently feel that these factors are not being fully leveraged in the Early Start Pension plan.

Criticism of fairness: When siblings benefit differently

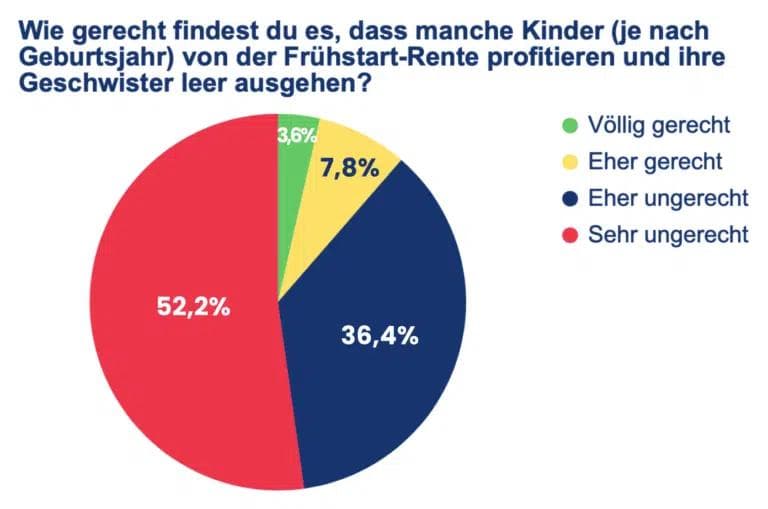

Figure 2: Perceptions of the fairness of the early retirement pension within families

Parents are particularly sensitive to the distributional impact of the early retirement pension. 88.6 percent consider it unfair or very unfair that children benefit depending on their year of birth, while older siblings get nothing.

This creates tension, particularly within families. Instead of promoting equal opportunity, the system is perceived as arbitrary—dependent on a child’s date of birth rather than actual need. For many parents, this is difficult to explain and undermines acceptance of the government’s social safety net.

Clarity as a Key Issue with Early Retirement

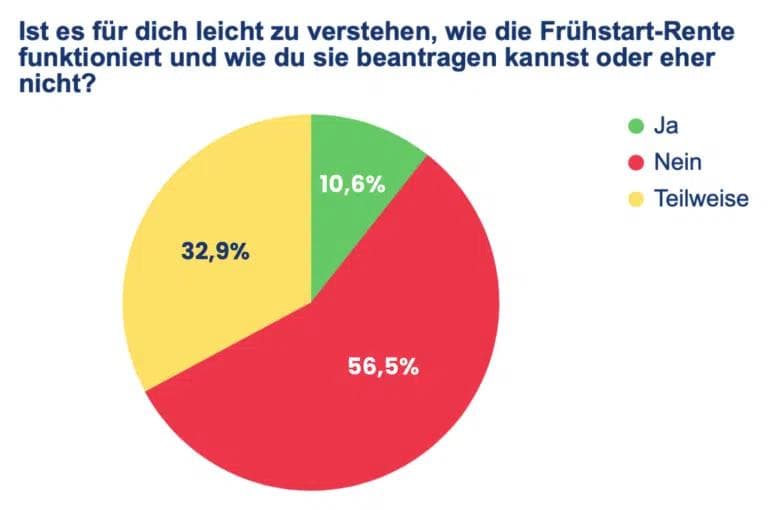

Figure 3: Parents' understanding of the early retirement pension

Another clear finding of the survey concerns the complexity of the model. Only 10.6 percent of parents say they fully understand how the Early Retirement Pension works and how to apply for it. 56.5 percent do not understand the model at all, and another 32.9 percent understand it only partially.

For a government retirement savings program that could affect millions of people, this is an alarming figure. Financial planning only works if it is transparent, accessible, and easy to understand.

Good idea, but the execution leaves something to be desired

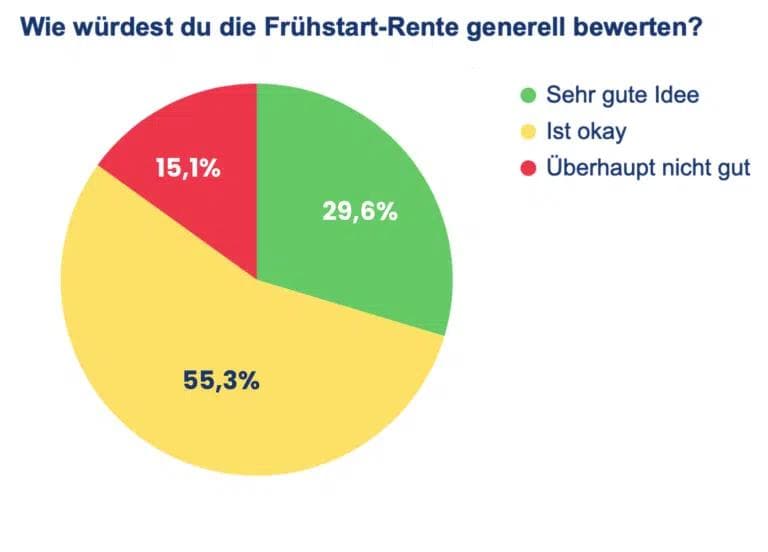

Figure 4: Parents’ Overall Assessment of the Early Retirement Pension

Despite all the criticism, the survey also shows that 85 percent of parents generally consider the idea of a government-sponsored pension plan for children to be a good one. At the same time, only 29.6 percent rate the specific design of the “Early Start” pension as “very good.” The majority see a clear need for improvement or reject the model in its current form.

Parents therefore make a clear distinction between the concept and its implementation and expect government pension plans to be designed in a way that makes economic sense.

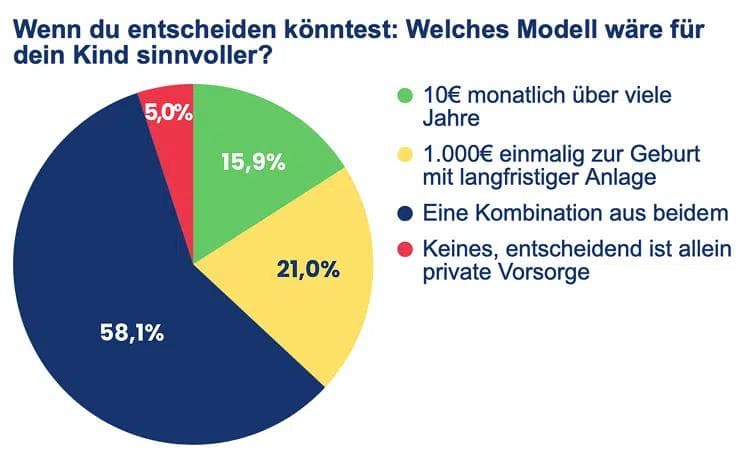

Which alternatives do parents prefer?

Figure 5: Preferred models for government support of wealth accumulation for children

It is particularly revealing to look at possible alternatives to the early retirement pension. Only 15.9 percent of parents would deliberately choose the €10-per-month option. A significantly larger number prefer:

- a one-time payment of 1,000 euros upon the birth of a child, with long-term investment, or

- by far the most common is a combination of government seed funding and ongoing support (58.1 percent).

This highlights a clear need to start earlier and take greater advantage of the power of compound interest.

Why the start date is more important than the grant amount

When it comes to building wealth for children, it is not just the amount of the investment that matters, but above all the point in time at which investing begins. Invest4Kids compared two scenarios in which the total amount is identical:

- From birth

- Contributions starting at age six, as provided for under the Early Retirement Plan.

The result is clear. Thanks to the extended effect of compound interest, investing from birth results in a return advantage of approximately 14,000 euros by retirement age. Simply starting earlier ensures that significantly more wealth is accumulated without requiring higher contributions.

This example illustrates why investing early is the key to building real wealth. This is also relevant from the government’s perspective. A one-time initial payment of 1,000 euros at birth would cost the government about 30 percent less in the long run than monthly subsidies spread out over several years, while providing significantly greater benefits for the children.

What parents are specifically calling for

In the survey, parents were able to contribute their own ideas on how the program could be improved. This resulted in numerous suggestions for improving the early retirement program:

- higher or dynamically adjusted grant amounts

- automatic payment without application

- sensible, cost-effective capital market investments

- greater integration with financial education

These points make it clear that parents are not opposed to government-provided social security per se. However, they expect a well-thought-out, fair, and understandable system.

Conclusion: The early retirement pension needs clear improvements

The results of the Invest4Kids survey clearly show that parents want government support in building wealth for their children. At the same time, they expect this support to be effective, fair, and easy to understand. If the Early Start Pension remains unchanged in its current form, many families believe it risks failing to achieve its goal.

Invest4Kids supports parents at this very stage with transparent advice, clear structures, and a long-term perspective on their children’s financial future.